By Eric Osiakwan

Chanzo is a Swahili word for “early stage” or “beginning,” a brand chosen by the firm to highlight our unique ability to help founders with smart new ventures into commercially viable businesses. So it came to pass that in the beginning, Angel Fair Africa (AFA) was a precursor to Chanzo Capital (CC).

After a successful critically acclaimed first AFA in Johannesburg, South Africa in 2013, which saw 24 startups pitch to a room of 68 investors with 3 deals closing during the event, the Africa Venture Capital Association (AVCA) incorporated AFA into their historic week of activities in Lagos, Nigeria in 2014.

RELATED: Chanzo Capital, TRIFIC SEZ, and ONESPACE launch COSSA Startup and Scaleup Accelerator

AVCA made provision for the hosting of the second AFA at the Intercontinental Hotel, 48 hours before their three-day summit, to which they gave us complimentary access. A number of AVCA delegates to AFA@2 chose to invest in the best-participating startups in their personal capacity.

That is when the idea of setting up a vehicle to accept third party capital came to me and with it the birth of Chanzo Capital. An Africa-focused tech venture capital firm investing in African founders that are building the digital economy by leveraging mobile web technologies to solve critical problems in their communities and society with potential coverage across Africa.

Mentor capital: Providing mentoring + funding

I started with the concept of mentor capital, which is providing mentoring together with the early-stage cheques I was writing to these founders. In most cases, I would mentor them for a while to build conviction before doubling down with a cheque. AFA served as breeding grounds for these founders because we would have them nominated by African innovation hubs, incubators and accelerators for our annual event.

As an ex-founder myself, I came to the craft of investing by focusing first on the founder(s) – building a relationship that engenders trust as the foundation for our engagement. Relationships take time to build, and so trust does not come fast. With trust comes the nucleus of conviction which also takes time. It is one thing to trust someone and an entirely different thing to build conviction that they can build a venture when in most cases they have never done it before. Mentoring therefore served as a bridge – made up of the steps that make for building conviction.

Once we have built conviction in the founder(s) or founding team that they could build the future they are projecting to us – i.e. the Total Addressable Market (TAM), we advance to the next stage of the ladder where we calculate the execution risk. Early-stage investing is a very risky enterprise – industry statistics show that nine out of every ten early-stage investments fail and one makes up for their sins. This was a shocking statistic that I first heard from my mentor, Esther Dyson who inspired me into investing.

Lying in bed that night, I told myself that I would try to make a dent in the startup high-failure phenomenon as I was not convinced that I wanted to make ten investments to get only one right. With that assumption came the prognosis that it had something to do with the execution risk.

Investors’ dilemma: The latency between vision and reality

In other words, there is a huge latency between vision and reality premised on the investors’ inability to calculate the execution risk they are taking. Over the ten years of our existence, we have come up with a formula for calculating the execution risk – that is our secret sauce which sits outside the remit of this essay.

Evidence of this formula is in our first set of sixteen investments from 2014, of which only five were unsuccessful – eleven are in business, of which five are profitable. We condition our founders to aim for profitability and not growth at all costs.

After calculating the execution risk, we take a leap of faith by deploying the capital and resources they need to get from vision to reality. The first iteration of that reality is a minimum viable product (MVP). An MVP is a preliminary version of a product, slightly more market-ready than a prototype.

Sometimes a prototype would suffice as an intermediate to an MVP. Building an MVP is an iterative process where you do an initial version, ship it off to the customer to use and wait for the customer to give you their feedback which you then incorporate into the next version of the product.

This process can go on for several rounds with the product improving at each iteration based on actual consumer feedback. This iterative feedback loop, when done well, leads to Product Market Fit (PMF) which leads to revenue generation and eventually cashflow.

Building a path to profitability

We subsequently focus the founder(s) on the unit economics of their business model to build a path to profitability, the basic principle being that the company needs to produce at price X and sell at price X + 1 – otherwise there is no sustainable business.

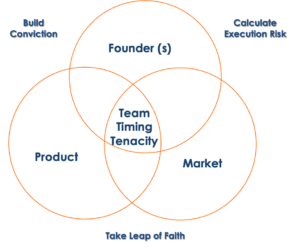

Chanzo Capital startup strategy execution framework

Our framework above in the diagram has timing and tenacity below the team making the 3Ts. Any startup is as good as the team behind it and the team must pay attention to the timing of the market. Sometimes the waves take longer to build up so the team needs tenacity – staying power – for the waves to build up so they can get on their board for a smooth surf. The 3Ts therefore form the centerfield of the model.

Over the ten years of our existence, we have mastered the art of building conviction, calculating the execution risk and taking a leap of faith with the team, then helping them to get the timing right which may sometimes require tenacity. We have used the framework to invest in another 24 startups since 2020 under covid, making a total of 35 startups in our portfolio. We have done these investments from three offices in Accra (Ghana), Nairobi (Kenya) and Johannesburg (South Africa) with our funds domiciled in Mauritius.

Focusing on the KINGS countries

We are a team of six with two staff members in each of the three offices with an additional 42 ex-founders, investors, venture builders and ecosystem players within our orbit. Our advisory board comprises of six members with a 50/50 gender parity. Our 35 portfolio companies are from Kenya, Ivory Coast, Nigeria, Ghana and South Africa making the KINGS countries in our first fund.

We expanded the second set of investments to include Uganda, Senegal, Tanzania, Zambia and Mozambique. These are the same countries we have taken the AFA event to in the last 11 years – investing on the back of the AFA footprint. To celebrate our 10th anniversary, we hosted an intimate dinner in Johannesburg, South Africa with some of our team members, advisors and partners. To the next ten years, cheers….:-)