By Max Cuvellier

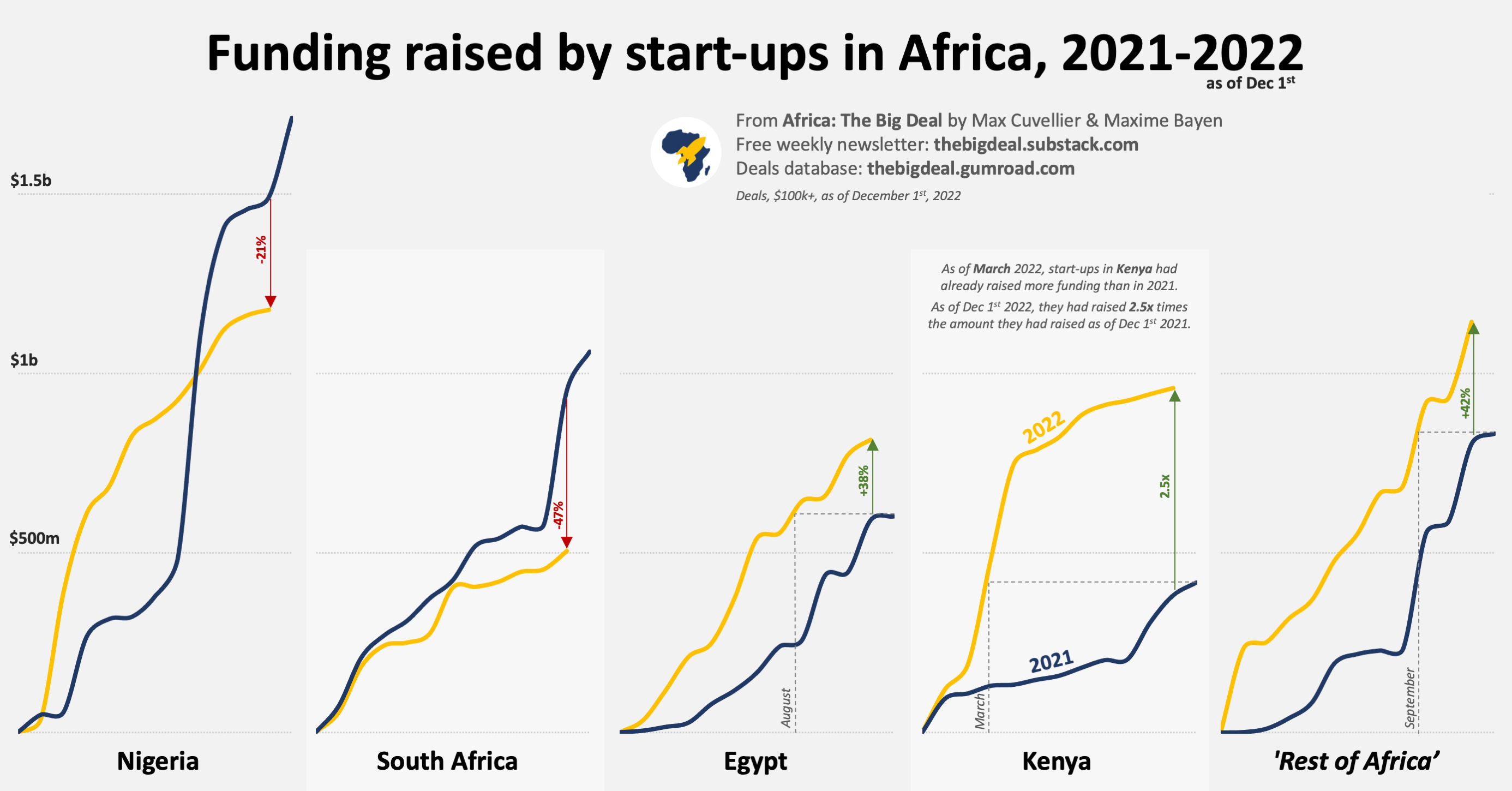

As we’re nearing the end of 2022, we take a closer look at how the Big Four (Nigeria, South Africa, Egypt and Kenya) fared in a tricky global context.

Was H1 the spring of hope, and H2 the winter of despair? Of course not. Things are never so black and white. The fact that funding slowed down dramatically in the second half of the year at the continent’s level hides strong discrepancies between ecosystems. It’s unlikely Algeria will complain about their H2, after Yassir’s $150m Series B last month.

RELATED: Amidst surge in global funding for African startups, NITDA assures Nigeria Startup Bill will become law

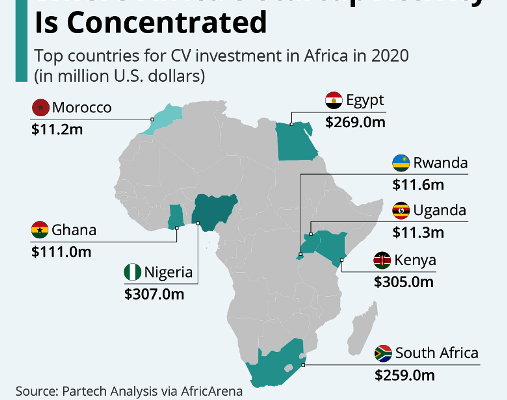

While for some, it was the best of times, for others it was the worst of times (and the Dickens references will stop right here, don’t worry). Let’s have a look at the continent’s Big Four who have attracted 75% of the funding in Africa this year so far (down from 82% in 2021):

|

- In Nigeria, after an incredible H2 2021, and a very strong H1 2022, H2 2022 has been much more quiet. In November only $16m of funding were announced, the lowest monthly number since June 2021. While Nigeria keeps the lead in absolute numbers this year (almost $1.2bn), the ecosystem would have to raise $534m in December to top its 2021 performance, as much as it raised in the past 7.5 months combined. It’s therefore extremely likely it will record a YoY decline in funding in 2022.

- Talking of decline, as of end of November South Africa had only raised about half of the funding it had raised at the same time last year. It would also take over half a billion dollars of funding announced in December – more than start-ups in South Africa have raised this year so far – to reverse the trend. It doesn’t help that November last year was quite exceptional, with two 9-digit rounds announced (Jumo and MFS Africa). Our bet is therefore that 2022 will be a year of double-digit decline in terms of funding.

- Things look much rosier for Egypt though, where funding raised in 2022 has tracked over the 2021 levels, month after month. By August, start-ups in Egypt had already raised more than they had in the whole of 2021 ($600m+), and they have now exceeded this number by 38%. Egypt has definitely emerged as one of the winners of 2022, especially as it was hit less badly than other ecosystems by the H2 slump.

- While it has been coasting in H2, Kenya has had such a strong start of the year that it had topped 2021 numbers by March, and already records 2.5x YoY growth between 2021 and 2022. Just a little push, and it could cross the $1bn mark. It is worth noting though that Kenya is really playing catch-up after a disappointing 2021: with -24% YoY, it was the only one of the Big Four to suffer a decrease in funding raised between 2020 and 2021, while its three peers were growing – exploding rather – by a factor of 4x to 5x.

What about the ‘rest of Africa’? It is obviously not at all a homogenous group, and once the 2022 numbers are in we’ll make sure to dive deeper, yet it is worth noting that funding overall has grown outside of the Big Four, +42% YoY already.

I don’t like to bet or gamble, but with a couple of weeks to go before the end of the year, it’s probably not so risky anymore… We’d love Nigeria and South Africa to prove us wrong and defy all odds in December though!

We’ll keep collecting the deals for the database until the very last day of the year, and be ready to analyse the hell out of 2022 for you in early Jan. In the meanwhile, this newsletter is taking a much-deserved break until the NYE fog clears. I hope you’ll also get a chance to let your hair down a bit! A bientôt

Credit: Africa: The Big Deal,